|

|

Post by kryptos2009 on Sept 2, 2010 21:43:30 GMT -5

Here is the PP Daily Thread (PPDT) data. XLF PP=14.17 MP=14.22 R1=14.27 MP=14.30 R2=14.33 MP=14.41 R3=14.49 MP=14.57 R4=14.65 MP=14.14 S1=14.11 MP=14.06 S2=14.01 MP=13.93 S3=13.85 MP=13.77 S4=13.69 O=14.07 H=14.22 L=14.06 C=14.22 FAS PP=20.20 MP=20.42 R1=20.64 MP=20.76 R2=20.88 MP=21.22 R3=21.56 MP=21.90 R4=22.24 MP=20.08 S1=19.96 MP=19.74 S2=19.52 MP=19.18 S3=18.84 MP=18.50 S4=18.16 O=19.82 H=20.45 L=19.77 C=20.39 FAZ PP=14.65 MP=14.75 R1=14.84 MP=15.01 R2=15.17 MP=15.43 R3=15.69 MP=15.95 R4=16.21 MP=14.49 S1=14.32 MP=14.23 S2=14.13 MP=13.87 S3=13.61 MP=13.35 S4=13.09 O=14.96 H=14.99 L=14.47 C=14.5 SPY PP=109.15 MP=109.48 R1=109.81 MP=109.98 R2=110.15 MP=110.65 R3=111.15 MP=111.65 R4=112.15 MP=108.98 S1=108.81 MP=108.48 S2=108.15 MP=107.65 S3=107.15 MP=106.65 S4=106.15 O=108.72 H=109.49 L=108.49 C=109.47 SPG PP=94.79 MP=95.43 R1=96.06 MP=96.41 R2=96.75 MP=97.73 R3=98.71 MP=99.69 R4=100.67 MP=94.45 S1=94.10 MP=93.47 S2=92.83 MP=91.85 S3=90.87 MP=89.89 S4=88.91 O=93.79 H=95.49 L=93.53 C=95.36 GS PP=139.46 MP=139.97 R1=140.47 MP=140.82 R2=141.16 MP=142.01 R3=142.86 MP=143.71 R4=144.56 MP=139.12 S1=138.77 MP=138.27 S2=137.76 MP=136.91 S3=136.06 MP=135.21 S4=134.36 O=139.93 H=140.15 L=138.45 C=139.78 JPM PP=37.95 MP=38.18 R1=38.41 MP=38.54 R2=38.66 MP=39.02 R3=39.37 MP=39.73 R4=40.08 MP=37.83 S1=37.70 MP=37.47 S2=37.24 MP=36.89 S3=36.53 MP=36.18 S4=35.82 O=37.84 H=38.2 L=37.49 C=38.16 MS PP=25.52 MP=25.69 R1=25.85 MP=25.94 R2=26.03 MP=26.28 R3=26.54 MP=26.79 R4=27.05 MP=25.43 S1=25.34 MP=25.18 S2=25.01 MP=24.75 S3=24.50 MP=24.24 S4=23.99 O=25.32 H=25.69 L=25.18 C=25.68 C PP=3.88 MP=3.91 R1=3.93 MP=3.96 R2=3.98 MP=4.03 R3=4.08 MP=4.13 R4=4.18 MP=3.86 S1=3.83 MP=3.81 S2=3.78 MP=3.73 S3=3.68 MP=3.63 S4=3.58 O=3.84 H=3.93 L=3.83 C=3.88 VIX PP=23.55 MP=23.75 R1=23.95 MP=24.33 R2=24.71 MP=25.29 R3=25.87 MP=26.45 R4=27.03 MP=23.17 S1=22.79 MP=22.59 S2=22.39 MP=21.81 S3=21.23 MP=20.65 S4=20.07 O=24.23 H=24.31 L=23.15 C=23.19 UUP PP=23.93 MP=23.94 R1=23.95 MP=23.98 R2=24.00 MP=24.03 R3=24.07 MP=24.10 R4=24.14 MP=23.91 S1=23.88 MP=23.87 S2=23.86 MP=23.82 S3=23.79 MP=23.75 S4=23.72 O=23.92 H=23.97 L=23.9 C=23.91 FROM: www.econoday.comEconomic Events & Analysis - 9/03/2010 Friday8:30 AM ET Employment Situation Released on 9/3/2010 8:30:00 AM For Aug, 2010 Prior Consensus Consensus Range Nonfarm Payrolls - M/M change -131,000 -90,000 -160,000 to 75,000 Private Payrolls - M/M change 71,000 40,000 -5,000 to 110,00 Unemployment Rate - Level 9.5 % 9.6 % 9.5 % to 9.7 % Average Hourly Earnings - M/M change 0.2 % 0.1 % 0.1 % to 0.2 % Av Workweek - All Employees 34.2 hrs 34.2 hrs 34.1 hrs to 34.3 hrs Market Consensus Before Announcement Nonfarm payroll employment in July declined 131,000 after falling a revised 221,000 in June and after a 432,000 boost in May. Of the July government plunge, 143,000 came from a drop in Census Bureau payrolls. State government fell 10,000 while local government dropped 38,000. Private nonfarm employment, which discounts the effects of hiring and firing temporary Census workers, accelerated moderately to a 71,000 increase, following a 31,000 gain in June. Average hourly earnings improved to up 0.2 percent, following no change in June. The average workweek for all workers rose to 34.2 hours from 34.1 hours in June. Turning to the household survey, the unemployment rate was unchanged at 9.5 percent in July. More recently, despite a dip this past week, initial jobless claims in August have been running higher than during July and this implies sluggish payroll and unemployment numbers. Employment indexes for the Philly and New York Fed manufacturing surveys were mixed as Empire rose while Philly slipped from positive to negative. Analysts will be tweaking their expectations with the ISM manufacturing and ADP reports just ahead of Friday's employment situation. Added Note: consensus numbers are revised as of Thursday afternoon. 10:00 AM ET Dennis Lockhart Speaks 10:00 AM ET ISM Non-Mfg Index Released on 9/3/2010 10:00:00 AM For Aug, 2010 Prior Consensus Consensus Range Composite Index - Level 54.3 53.0 52.0 to 54.5 Market Consensus Before Announcement The composite index from the ISM non-manufacturing survey in July improved to 54.3 from 53.8 month before. Yet business activity, akin to a production index, edged lower to a still very strong 57.4 – well above breakeven of 50. But we could see a higher composite in August as the new orders index rose nearly 2-1/2 points to 56.7. Additional World wide Economic Calendar information can be found at the following website. worldeconomiccalendar.com/NOTE: The previous days OHLC data for todays PPDT was gathered from finance.yahoo.com for each individual stock by a series of webquerys built into a spreadsheet. The formulas used by the www.mypivots.com website to create the Pivot Points were found in the sites help files. The formulas were built into the spreadsheet which acts on the previous days OHLC data gathered from Yahoo. The Pivot Points were created using the formulas from www.mypivots.com but NOT by using the site. Please let me know if you find any errors in the data. Use of this data is at your own risk. |

|

|

|

Post by jack on Sept 2, 2010 21:51:30 GMT -5

Thx Krypt ;D

...turnin' in kids - seeya on the flip

;D

|

|

|

|

Post by brosin on Sept 2, 2010 23:11:35 GMT -5

Elle, where are you?

|

|

|

|

Post by brosin on Sept 2, 2010 23:40:43 GMT -5

Courtesy of Brian Shannon at Alphatrends Caldaro: Caldaro:Overnight the Asian markets were all higher. Europe opened higher but closed mixed. US index futures were relatively flat overnight, and at 8:30 weekly Jobless claims were reported about flat: 472K v 475K. Also, Productivity declined: -1.8% v -0.9%, while unit Labor costs rose: +1.1% v +0.2%. At 9:00 FED chairman Bernanke testified before the senate: www.federalreserve.gov/newsevents/testimony/bernanke20100902a.htm. The market opened flat, around SPX 1080, but rallied to 1087 and the 1090 pivot range by 10:00. At this time Factory orders were reported positive: +0.1% v -1.2%, and Pending home sales rose: +5.2% v -2.6%. The market then pulled back to SPX 1082 by 10:30. For the next several hours the SPX stayed in a narrow trading range while drifting higher. Then, in the last couple of hours the SPX took out the 1087 high and move higher to close at exactly 1090. For the day the SPX/DOW were +0.70%, and the NDX/NAZ were +1.10%. Bonds lost 9 ticks, Crude gained $1.10, Gold added $5.00, and the USD declined. Support for the SPX remains at 1058 and then 1041, with resistance at 1090 and then 1107. Short term momentum remained overbought throughout the day. Something we have not seen in quite a while. Tomorrow, the monthly Payrolls report and Unemployment rate at 8:30, then ISM services at 10:00. The rally off of tueday's SPX 1041 low continued today. The SPX is now right at the 1090 swing pivot we have been tracking for what seems like months. Remember, this market has traded between the 1041 pivot and the 1136 pivot, spare one week, since mid-May. Short term OEW charts remain positive. The key areas to watch are this pivot and the SPX 1100 level on the upside, then, the 1058 and 1041 pivots on the downside. The hourly RSI has now stayed overbought for two days, and the daily RSI is approaching overbought. Tomorrow, the often market volatile Payrolls report. Should be an interesting day before the three-day, end of summer, holiday weekend. Cobra: The bottom line, the short-term trend is up, I closed long position added today before the market close but still hold partial long entered on 09/01. Slightly bearish biased toward tomorrow, at least don’t expect the market to up more than 1% because TICK closed above 1,000 again. Tomorrow is Non Farm Payroll day again. I’ve mentioned lots about the usual pattern of this day – open high may close lower while open low may close higher. For more details please take a look at 08/05 Market Recap. The only thing I want to remind you is if unfortunately a red day tomorrow, then be careful about a possible trend change as my next pivot date around 09/07 to 09/10 may indeed come true. The chart below is interesting because it was exactly the same I mentioned on 08/05 Market Recap: If gap down unfilled tomorrow then the gap will be filled within days because back to back unfilled gaps are very rare, at least not seen on the chart below. Therefore if indeed we have a gap down unfilled tomorrow which as mentioned above could mean a possible trend change (since it automatically means a red day), no need to worry, because the gap will be filled very soon which guarantees that bulls will have chances to escape unharmed. (CHART TOO BIG: CLICK TO SEE; TALKS ABOUT DEFINITION OF FILLED GAPS) lh4.ggpht.com/_APmrYvpA45s/TIBBd-OYbwI/AAAAAAAAIf4/wCbfbXDV4HA/SPYUnfilledGaps_thumb.png?imgmax=800Bespoke:Best Performing Russell 3,000 Stocks Year to DateThe Russell 3,000 makes up about 98% of the US equity market, and below we highlight the stocks in the index that are up the most so far in 2010. These names are all up 100% or more year to date. With a third of the year left, Wabash National (WNC) holds onto the top spot with a gain of 265.08%. Somaxon Pharmaceutical (SOMX) ranks second at 253.70%, while Applied Energetics (AERG), IDT Corp (IDT), Acme Packet (APKT) and Isilon Systems (ISLN) are the rest of the names with YTD gains of more than 200%. The most recognizable name on this list is probably NetFlix (NFLX), which is currently up 150.32% in 2010. A few other noteworthy stocks on the list of big winners include Crocs (CROX), 3PAR (PAR), MBIA (MBI), OpenTable (OPEN), and Las Vegas Sands (LVS). It will be interesting to see how much this list changes by the end of the year. How Bad is the First Friday of September?We've heard some commentary today noting that the first Friday of September has typically been a rough day for the market. We went back and looked at the Dow's performance on all of the first Fridays of September since 1900 to see what the numbers actually look like. Below is a list of all of them. As shown, the average change for the Dow on all 109 days since 1900 has been +0.22%. This is pretty positive considering the average change for all days since 1900 has been about +0.03%. The median change is strong as well at +0.21%. The worst first Friday of September came in 2001 when the Dow declined 2.39%. The best first Friday of September came in 1932 when the index climbed 4.21%. Over the last 10 years, the index has been up 5 times and down 5 times on these days, and the index was up 1.03% on the first Friday of September last year. So really, the first Fridays of September haven't been that bad at all. Employment Report StatsAhead of tomorrow's employment report we wanted to highlight some interesting trends ahead of the release. The first chart below highlights the average magnitude of the surprise in non farm payrolls (NFP) relative to expectations for each month of the year. For this chart, we took the absolute average of the difference between the actual and estimated change in NFP for each month since 1998. As shown in the chart, reports in September (for month of August) are actually where economists have been closest to estimating the actual change in NFP. On average, economists either under or overestimate the actual number by 46K. The next closest month is November (for month of October) where the average margin of error is 58K. October has historically been the worst month for economists in predicting the change in NFP for the prior month. The consensus forecast for reports released in the month of October are typically 80K above or below the actual reported number. In terms of the average performance of the S&P 500, the index has risen an average of 0.11% on the day of the August employment report (released in September). This puts September right in the middle in terms of performance on NFP fridays. |

|

|

|

Post by brosin on Sept 2, 2010 23:43:46 GMT -5

Following 3 links courtesy of Barry Ritholtz at the Big Picture(*trust me when I say I would not post this much reading if my hands weren't tied; they were all so good) Dick Fuld’s Fantastic Revisionism ! “Lehman was forced into bankruptcy not because it neglected to act responsibly or seek solutions to the crisis, but because of a decision, based on flawed information, not to provide Lehman with the support given to each of its competitors and other nonfinancial firms in the ensuing days.” -Richard S. Fuld Jr., Lehman Brothers former chief executive (NYT) > The fantasy world inhabited by Lehman Brothers CEO Richard Fuld was given a surprisingly sympathetic ear from an unexpected forum yesterday: The Financial Crisis Inquiry Commission. This is a deeply disturbing development, as it leads to the unfortunate suspicion that the FCIC does not have the slightest clue as to the causes of the housing collapse, recession and and market crash. There are two issues here: The first is “why did Lehman collapse?” The second is “Why didn’t the Fed rescue them?” Let’s look at both. I’ve spilled far too many pixels explaining why Lehman crashed and burned, but for those of you who may have forgotten: 1. Under-capitalized, over-leveraged: Lehman Brothers was the biggest bankruptcy in US history. To avoid that fate, LEH mneeded to be sufficiently capitalized, and use only moderate leverage (LEH embraced 40 to 1 leverage). Rather than have a sufficient capital base, the bank chose instead to chase profits: A greater capital cushion meant less underwriting activity, smaller gains, greater risk. The downside of having a de minimus capital structure is when bad investments are made, there is no room for error. 2. Bad Modeling Assumptions: LEH made numerous false assumptions in their econometric models: a) Residential RE never goes down; b) The derivatives market is always liquid, with ready buyers available; c). We can always borrow short and lend long with no liquidity concerns; There was substantial evidence and warnings that ALL of these assumptions were false, but they were ignored by management as a risk to profits. 3. Excess RE Exposure: Lehman was the biggest securitizer of mortgages on Wall Street. They underwrote more mortgages than any other bank on Wall Street. By 2004, LEH was originating $40B per year in mortgages to feed their own CDO machine (which as Roger Lowenstein has pointed out, was more lucrative than the stock and bond business). 4. Reliance on Ratings: Lehman’s entire business model was predicated on the ratings of Moody’s and S&P being reliable. However, LEHMAN was one of the prime purveyors of credit rating payola — they were paying the NRSROs a fee to slap a Triple AAA rating on junk paper. If they did not know the credit ratings were utterly worthless, they sure should have. 5. CDO Ownership: Lehman kept the senior-most layers of CDOs they created for themselves, but bought credit default swaps on them “for safety.” Consider that they were not confident enough of the models which forecast the solvency of those tranches, yet they used the same models to determine AIG was a credit worthy counter party to insure them. That’s why LEH collapsed, and it was apparent (at least to us) back in June 2008 they were in trouble. Why did the Fed not save them? There were several reasons: 1. One off: The Bear Stearns bailout was supposed to be a “one of a kind,” not the start of a series of rescues. The Fed hoped to hold the line at only one such taxpayer backed rescue. The fear was if they did a 2nd, they could not say no to the rest of the Street. Lehman was in effect the Fed’s Maginot Line (it also was out flanked and rendered strategically useless). 2. Fed Overreach: Bernanke was widely criticized for the Bear rescue as a huge overstep of authority. Even former Fed Chair Paul Volcker overcame the inherent reluctance of formerFOMC chairs to to criticize sitting Fed heads to express his concern about the over reach and power grab. 3. No to Private Rescue: Dick Fuld turned down a private rescue just months earlier. Warren Buffett offered Fuld billions, plus the equivalent of the Berkshire Hathaway Good corporate Housekeeping seal of approval. FULD TURNED BUFFET DOWN. How could the Fed, in good conscience, bail out a firm that refused to accept a Buffett rescue? Indeed, his terms for LEH were far more generous than what BRK ultimately offered Goldman Sachs and GE. 4. Insolvent: Lehman books are why a loan never happened. LEH was essentially insolvent, with liabilities that vastly outweighed what few assets there were. This insufficiency is why a loan was simply not possible — it was considered a guaranteed loss. 5. Moral Hazard: How much of a clusterfuck must any financial firm be before a rescue is deemed an outrageous moral hazard? For the 3rd and 4th reasons above, Lehman was believed to be “Beyond rescuing.” And it was due to the specific choices Lehman’s management made. To think that Fuld’s brand of psychopathic revisionism was given a sympathetic hearing is deeply disturbing. I haven’t written this before, but now I am compelled to: I now fear the FCIC report is going to be an ideological farce. The nightmare report scenario is a collection of false statements, half truths, misunderstandings, confirmation biases, and rhetorical nonsense. |

|

|

|

Post by brosin on Sept 2, 2010 23:45:15 GMT -5

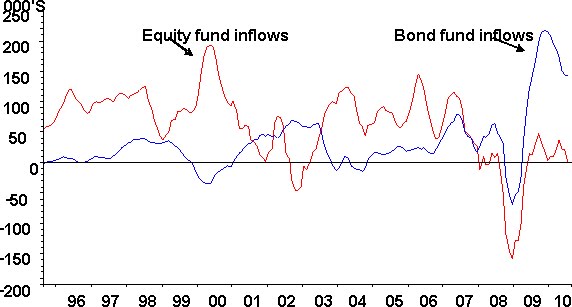

Bond bubble: A Sterile Debate on SemanticsMuch ink has been spilt over the question of whether government bonds are in a bubble or not. The bond bubble believers love to cite stats along the lines that bonds are witnessing inflows at the same pace as equity funds did during the TMT bubble.  The bond lovers respond an asset with a finite life and no hope of limitless capital gain can’t really be a ‘bubble’, and beside they argue the ‘fundamentals’ warrant current valuations. (i.e. inflation is low and will remain so). However, to me this is largely a sterile debate over semantics. The issue shouldn’t be whether bond are a bubble or not, but rather are bonds a good investment or not? Ben Graham defined “An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative”. Do bonds offers long term investors a sensible level of return? I’ve always thought that in essence bond valuation is a rather simple process (at least one level). I generally view bonds as having three components: the real yield, expected inflation and an inflation risk premium. The real yield can be measured in the market thanks to inflation-linked bonds. In the US, a 10 year Tip is trading at just under 1%. Expected inflation can be assessed in a variety of ways. We could use surveys, for instance, the Survey of Professional forecasters shows an expected inflation rate of just under 2.5% p.a. over the next decade. In contrast, the nominal bonds minus the TIP yields implies a figure of more like 1.5% p.a. The inflation swap market is implying a 2% p.a. inflation rate over the next ten years. The inflation risk premium (a risk premium to compensate for the uncertainty of future inflation) is generally held to be between 25bps and 50bps. Given the uncertainties surrounding the impact of monetary and fiscal policy I’d argue that using the high end of that range seems reasonable. Using these inputs a ‘fair value’ under normal inflation would be around 4%. Of course, this assumes that the current market 1% real yield is itself a ‘fair price’. This seems like a questionable assumption to me. In the UK we have a longer history of index linked bonds – introduced in 1986. The average yield since the introduction is 2.6%, in the last decade the average real yield has been 1.5%. Given this ‘parameter’ uncertainty is would be reasonable to say that ‘fair value’ for 10 year bonds is somewhere in the range of 4-5%. The current 2.5% yield on the US 10 year bond is clearly a long way short of this. So unless you believe that Japan is correct template for the US (i.e. inflation will be zero for the next decade), government bonds don’t offer an attractive return as a buy and hold proposition. Another way of looking at this problem is to ask how much weight the market is putting on a ‘Japanese’ outcome. Let’s assume three states of the world (a gross simplification, but convenient). In the ‘Normal’ state of the world bonds sit at close to equilibrium, say 4.5%. Under a ‘Japanese’ outcome yields drop to 1%, and under an inflation outcome yield rise to 7.5% (this assumes a 5% inflation rate). The table below lays out my own estimates (kind of an agnostic view, with a prior biased towards the ‘Normal’ but cognizant of the other two risks), then bond should yield around 4.4%. I can then tinker around with the probabilities to generate something close to the market’s current pricing. In essence, the market is implying a 70% probability that the US turns Japanese. Bond Yield JM Probabilities Market implied Normal 4.5 0.5 0.2 Japan 1 0.25 0.7 Inflation 7.5 0.25 0.1 Expected Yield 4.4 2.4 It is possible to build a speculative case for bond investment (i.e. riding the deflationary news flow down), however, as ever this leaves participants with the conundrum of Cinderella’s ball as described by Warren Buffett “The giddy participants all plan to leave just seconds before midnight. There is a problem though: They are dancing in a room in which the clocks have no hands!” Personally I prefer to stick to investment rather than speculation.

|

|

|

|

Post by brosin on Sept 2, 2010 23:50:38 GMT -5

Interest Rates: 60-Year CycleLast week, we reviewed the History of US Interest Rates: 1790-Present via Doug Kass. Following that Stephen (of Wells Fargo Advisors) pointed us to this fascinating 60 year cycle in interest rates. It is quite compelling, to say the least:

|

|

|

|

Post by ask2lern on Sept 3, 2010 6:23:19 GMT -5

Thanks for the info Kryptos and Bros ……….Here are the pivots……….…hope everyone has a great day …………………GLTA

GOLD

R4 1277.23

midpoint 1272.83

R3 1268.43

midpoint 1264.03

R2 1259.97

Midpoint 1257.80

R1 1255.97

midpoint 1253.40

PP 1250.83

midpoint 1249.00

S1 1247.17

midpoint 1244.60

S2 1242.03

midpoint 1237.63

S3 1233.23

midpoint 1228.83

S4 1224.43

SILVER

R4 20.51

midpoint 20.36

R3 20.21

midpoint 20.06

R2 19.91

midpoint 19.85

R1 19.79

midpoint 19.70

PP 19.61

midpoint 19.55

S1 19.49

midpoint 19.40

S2 19.31

midpoint 19.16

S3 19.01

midpoint 18.86

S4 18.71

IMW

R3 64.74

R2 64.06

R1 63.63

PP 62.95

S1 61.52

S2 61.84

S3 61.41

TNA

R4 44.20

midpoint 43.22

R3 42.24

midpoint 41.26

R2 40.28

midpoint 39.90

R1 39.52

midpoint 38.92

PP 38.32

midpoint 37.94

S1 37.56

midpoint 36.96

S2 36.36

midpoint 35.38

S3 34.40

midpoint 33.42

S4 32.44

TZA

R4 38.63

Midpoint 37.74

R3 36.86

midpoint 35.97

R2 35.09

midpoint 34.54

R1 33.98

midpoint 33.65

PP 33.32

midpoint 32.77

S1 32.21

midpoint 31.88

S2 31.55

midpoint 30.66

S3 29.78

midpoint 28.89

S4 28.01

SDS

R3 33.68

R2 33.48

R1 33.07

PP 32.87

S1 32.46

S2 32.26

S3 31.85

………………………..GLTA

|

|

|

|

Post by ask2lern on Sept 3, 2010 6:25:13 GMT -5

From http://www.optionmonster.com..................GL

Indexes above resistance

September 3, 2010 Fri 5:10 AM CT

A late-day push drove the indexes above resistance before key economic data is released Friday morning. The 50-day moving averages that were resistance are now support. The secondary resistance levels are now first resistance.

Nasdaq 100 (NDX)

First support is at 1830.28 -- the 50-day moving average. On a breakout, the 200-day moving average at 1862.37 would be next resistance.

For the NASDAQ 100 Index Tracking Stock (QQQQ) first support is at $44.99. First resistance is at $45.81.

S&P 500 (SPX)

First support is at 1081.27 -- the 50-day moving average. First resistance is at 1100, with the 200-day moving average at 1115.64 as next resistance.

For the Standard and Poor's Depository Receipts (SPY) first support is at $108.35. First resistance is at $110, and thereafter at $111.79.

Russell 2000 (RUT)

First support is at 627.53 -- the 50-day moving average. First resistance is now at the 200-day moving average, last at 644.47.

For the iShares Trust Russell 2000 Index Fund (IWM) first support is at $62.77. First resistance is at $64.48.

By: Bryan McCormick

|

|

|

|

Post by ask2lern on Sept 3, 2010 6:26:46 GMT -5

From http://www.optionmonster.com.......................GL

Jobs and services on the docket

September 3, 2010 Fri 5:08 AM CT

Two reports today have the potential to move stocks. The first, the Employment Situation Report, has been eagerly awaited all week. The second, the ISM Non-manufacturing Index, hasn't received as much attention but has the potential to surprise in the same way the ISM Manufacturing Index did earlier this week.

The employment report, due at 8:30am eastern time, has several components. The headline number is expected to show a drop of 100,000 jobs. The range varies widely from a loss of 197,000 to a very bullish gain of 87,000. Traders to some degree are expecting bad news on the headline. Most attention will focus on private payrolls sub-component, which is expected to grow by 41,000. Once again, the range is very wide from a bearish loss of 17,000 a wildly optimistic gain of 120,000 at the high. Those numbers come from the part of the report known as the establishment survey.

The household survey includes the headline unemployment rate, which is expected to be 9.6 percent. Forecasts range from a bullish 9.5 percent to to a bearish 9.8 percent. It would be particularly negative if the unemployment were to approach or surpass 10 percent.

The ISM Non-manufacturing Index will be released at 10 a.m. eastern. Consensus calls for the index to drop to 55.9, from the previous 57.4. The range is from a bearish 54 to a bullish 58.

By: Bryan McCormick

|

|

|

|

Post by ask2lern on Sept 3, 2010 6:50:02 GMT -5

From www.optionmonster.com .......................................GL A tale of two volatilitiesSeptember 2, 2010 Thu 12:21 PM CT The VXX Short Term VIX futures ETN has dropped to the lowest level since April, even though the volatility index it tracks is little changed in the last four weeks. The VXX trades at $20.23, down another 1.94 percent on the day. It has fallen 16 percent in the last seven sessions, and 44 percent from its late-May high. It is now below the level from the May 6 “flash crash”, but that hides the true level of volatility.  Uploaded with ImageShack.usThe VIX is down 1.21 percent to 23.60, near its lowest reading since Aug. 10. It would have to fall below 18 to return to the same April range VXX. Furthermore, the VIX is simply the 30-day projection of volatility. VIX futures, which are a snapshot of where traders think the VIX will be in the future, are even higher. The September futures trade at 25.35, with October at 29.3 and November and December both above 30. The VXX is a constantly rolling combination of the front two month futures. Given the upward sloping term structure on VIX, it consistently sells a cheap first first month to buy a more expensive second month, from one expiration to the next -- an expensive proposition. So the lower VXX really doesn’t speak to any sort of “complacency”. Actually the opposite is true to some degree because it means fear is still elevated in the longer term. Finally, those who were excited about the rollout of the XXV Inverse VIX Short-Term Futures ETN as a way to get short the VXX may be a bit disappointed. I haven’t done a thorough analysis yet, but it certainly appears that a simple short position in VXX outperforms owning XXV position by quite a bit. That may be the reason we have seen a big synthetic short position go off in the VXX options out in January of 2012. (Chart courtesy of tradeMONSTER) By: Chris McKhann |

|

|

|

Post by abdogman on Sept 3, 2010 7:29:06 GMT -5

Bros,Ask,Kryptos thx for nmbrs and info ....

Bros -Great Posts ....Exalt!!

Good Luck and Good Morning Gang...........BFTO!

|

|

|

|

Post by ccash04 on Sept 3, 2010 7:46:37 GMT -5

Morning guys, thanks for the info

Nice move after the jobs number, will be interesting to see if it can continue to hold or rise through out the day..

TLT broke thru 104 and now is at 102.80 quickly looking like its going to fill the gap this morning.. I will be selling the TBT 33 calls from yesterday morning.

|

|

|

|

Post by brosin on Sept 3, 2010 8:05:59 GMT -5

Morning all - saw futures and had to get up and moving a little earlier here today. I cannot say I am not very pleased to see 1100+ was hit in futures

|

|

|

|

Post by abdogman on Sept 3, 2010 8:33:41 GMT -5

xlf 14.44 on 1m

|

|

|

|

Post by ccash04 on Sept 3, 2010 8:34:34 GMT -5

Sold TBT 33 calls @ .99 bought at .56  |

|

|

|

Post by deadmoney95 on Sept 3, 2010 8:36:01 GMT -5

Wow. Morning all. Thanks as always for the info. Nice move up in the Road to OPEX, Jack!

Carl F's take on the day:

September S&P E-mini Futures: Today's range estimate is 1092-1108. The ES is headed for 1140 and higher

|

|

|

|

Post by ccash04 on Sept 3, 2010 8:36:08 GMT -5

Over 1100 on ES

|

|

|

|

Post by abdogman on Sept 3, 2010 8:38:17 GMT -5

xlf 14.48 on 1m

|

|

|

|

Post by abdogman on Sept 3, 2010 8:41:31 GMT -5

xlf 14.505 on 1m

|

|

|

|

Post by ccash04 on Sept 3, 2010 8:43:06 GMT -5

Weekly option holders (long) would have made or lost a sh*t-ton of money this week.

|

|

|

|

Post by jack on Sept 3, 2010 8:44:25 GMT -5

XLFs macd crossed neg on the 1min w/ BBs tightening

(Good morning Rog!)

|

|

|

|

Post by abdogman on Sept 3, 2010 8:44:49 GMT -5

macd on 1m xlf fas neg now

xlf 14.48 on 1m

|

|

|

|

Post by jack on Sept 3, 2010 8:46:00 GMT -5

macd on 1m xlf fas neg now xlf 14.48 on 1m ;D |

|

|

|

Post by abdogman on Sept 3, 2010 8:47:31 GMT -5

XLFs macd crossed neg on the 1min w/ BBs tightening (Good morning Rog!) To You as Well!! |

|

|

|

Post by brosin on Sept 3, 2010 8:50:04 GMT -5

Volume is pretty damn big here to start, I wonder if its not everyone selling into it and taking the rest of the weekend off. If that's the case, hell, if we stay up here, that'd be a great sign.

|

|

|

|

Post by ccash04 on Sept 3, 2010 8:50:57 GMT -5

Less than 1% to go until MU reaches the +10% level since 9/1 |

|

|

|

Post by abdogman on Sept 3, 2010 8:52:30 GMT -5

xlf 14.47 and sideways between tight BB's

|

|

|

|

Post by ccash04 on Sept 3, 2010 8:55:49 GMT -5

Hope this ISM number doesn't mess anything up.

|

|

|

|

Post by abdogman on Sept 3, 2010 9:01:29 GMT -5

xlf 14.43 on 1m

|

|